Quantifeed Wins Deloitte Technology Rising Star Award 2023

We are proud to announce that Quantifeed has been awarded the prestigious 2023 Deloitte Technology Rising Star Award.

We are proud to announce that Quantifeed has been awarded the prestigious 2023 Deloitte Technology Rising Star Award.

We are proud to announce our latest Series C funding round led by HSBC Asset Management’s (HSBC AM’s) alternative investments business, HSBC Alternatives.

Today we launch an updated look and feel of our brand. This is the ideal introduction to who we are and what we do.

The ET Net Fintech Awards aims to commend the good use of fintech practices and recognise outstanding Hong Kong-based companies.

On 29 November 2021, the Quantifeed team accepted the FinTech Award at the HKCEC. The ceremony was attended by leading and upcoming ICT talents and

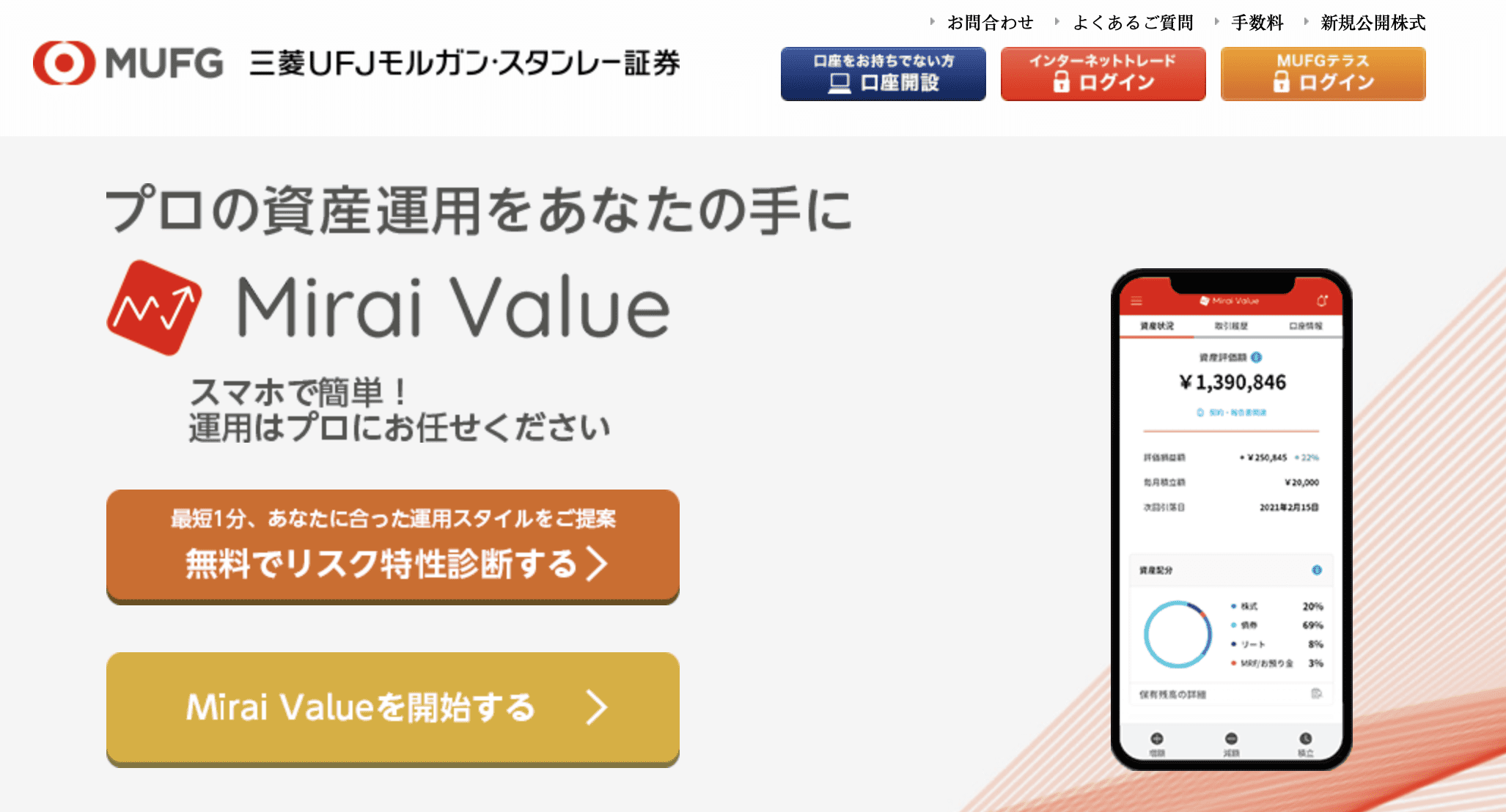

Quantifeed, Asia’s leading provider of digital wealth management solutions, has partnered with Mitsubishi UFJ Morgan Stanley Securities Co., Ltd (MUMSS) to launch Mirai Value, a smartphone-based discretionary investment service.

It’s an honour to be nominated for the Metro Finance Impetus Award in the wealth management category. Thank you to our clients, partners and investors for your continuous support!

Quantifeed is delighted to be named as “Outstanding B2B Robo-advice Platform 2020” at the ET Net Fintech Awards for the second year in a row.

HONG KONG digital wealth management solutions provider Quantifeed has raised an undisclosed amount of funding from its Series B+ round led by global asset manager Franklin Templeton.

When you visit any web site, it may store or retrieve information on your browser, mostly in the form of cookies. Control your personal Cookie Services here.